By Adam Stein and Deric Tilson

The Trump administration has announced, through multiple executive orders and statements, its intention and goal to ensure energy dominance through enabling nuclear energy. But the goal of deploying nuclear energy and having policies in place to ensure its success are not the same. On Monday, the House Ways and Means Committee released “The One, Big, Beautiful Bill,” detailing its plans to phase out many of the tax credits and subsidies originating in the 2022 Inflation Reduction Act. Many of these credits, including Sections 45U, 45V, 45Y, 48C, and 48E, benefited nuclear energy directly. Senate Republicans have already signaled that this bill would need changes to pass.

Regardless, it raises the question:

Would the end of the IRA credits end all hope of building new nuclear energy?

The repeal of the existing tax credits would not ring the death knell for a nuclear resurgence, but it would remove the scaffolding supporting its construction.

The Role of Tax Credits and Monetary Incentives

The preservation of IRA credits is synonymous with maintaining momentum in the fight against climate change. The IRA credits, particularly the Production Tax Credit (PTC) and Investment Tax Credit (ITC) applicable to nuclear, help level the playing field against subsidized renewables and compete against historically cheaper fossil fuels by lowering the cost of nuclear projects. They provide the financial certainty needed for the long and capital-intensive process of developing new nuclear projects, including next-generation small modular reactors (SMRs) and other advanced designs. With these credits, the pathway to achieving ambitious decarbonization goals by mid-century appears more viable, supporting a diverse clean energy portfolio where nuclear plays a foundational role in grid stability and emissions reduction.

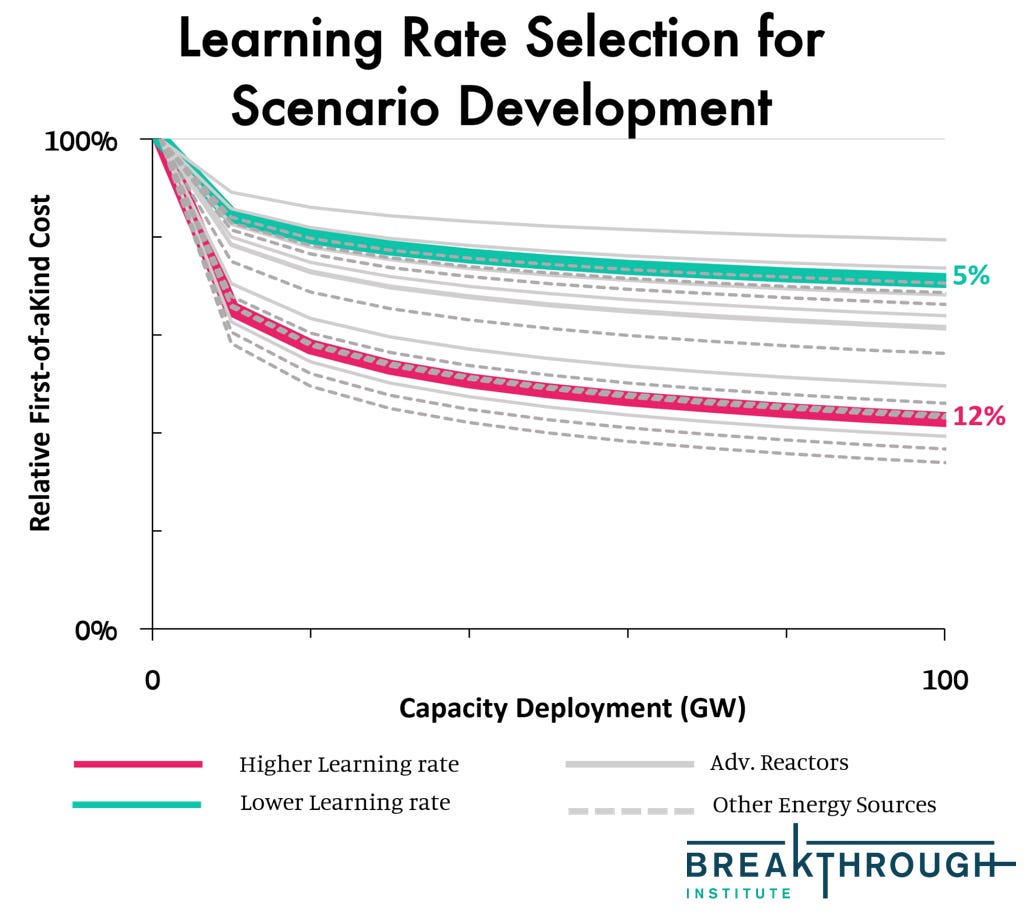

First-of-a-kind (FOAK) technologies almost always need early support as they are in direct competition with established technologies. This is an area where the government can and has historically contributed to the advancement of technological innovation. Early support, especially in the realm of basic research, provides multiplying and sometimes compounding benefits to society. Private firms do not always have the large amounts of capital or the long time horizons necessary to engage in basic research; Bell Labs was an exception among firms, but that was predominantly due to its monopoly status, resulting in excess profits.

Government support for research can come in a variety of forms, ranging from grants to subsidies to tax credits. Grants tend to be the earliest stage of support and are more focused than later forms of support. Applicants apply for such programs, and the federal agency chooses the winners. Grants usually have specific criteria and expectations for their dispersal; the federal agency awarding the grant expects to have some oversight when it provides funds. Demonstration plants for TerraPower X-Energy are supported by grants under the Advanced Reactor Demonstration Program. Recently, the current administration celebrated new grants for HALEU research and production, and Gen 3+ SMRs. Subsidies vary in specificity and government involvement. Tax credits tend to shift more control to the market and significantly shorten or eliminate approval timelines.

As long as the technology is young and continues to show signs of potential benefits, it makes sense for the government to continue subsidizing and engaging in research, but as the technology matures, firms begin to make investments and the technology becomes commercially viable, the government should pare back its subsidies. Subsidizing mature technologies distorts market signals, creates inefficiencies, and chooses winners. This reduces innovations that might have otherwise happened and constrains the path of technological progress.

Solar and wind credits have persisted over the past two decades, even as the technologies have matured and pushed out investment for other forms of energy generation. Nuclear does not need subsidies to operate effectively, but it is unclear whether FOAK nuclear will be competitive with natural gas, regardless of renewable subsidies. In some markets, especially those whose interconnection queues are filled with renewables, nuclear subsidies are needed because wind and solar subsidies have continued even after they became commercially competitive, and those subsidies create an anticompetitive playing field within the market. Efficient price signals are no longer being sent out; the price signals have been distorted. The distortion makes it difficult to extract a signal from the noise.

“The One, Big, Beautiful Bill” calls for the phase-out of investment and production tax credits across renewable and clean-energy technologies, not just nuclear. The phase-out reduces the price signal distortion at the electricity market level, but without another policy driver, investments may be more muted. That will slow deployment significantly. We will still have first movers that are procuring due to their own goals, but without the PTC and ITC, nuclear has less of an advantage moving forward.

Non-Monetary Policy Drivers

Not all industrial and innovation policy is based on economic incentives.

Before the IRA was passed and the tax credits implemented, Breakthrough Institute published the Advancing Nuclear Report, exploring how advanced nuclear could reach scale. The study found that a large scale up of nuclear energy would result in a lower-cost and reliable energy system, and was robust across a range of costs. However, those results were in the context of decarbonizing the grid, and there is no current federal mandate to hit a net-zero emission energy system to provide the necessary market driver. There is similarly no direct mandate at the federal level for national security, energy dominance, or fuel with regards to a nuclear energy resurgence. Although there is a small mandate for the federal government to buy renewable energy.

The Inflation Reduction Act, while having many subsidies and pecuniary mechanisms, was largely a symbolic piece of legislation announcing the United States’ commitment to clean energy investments and emissions reductions. With the reconciliation bill removing key parts of the IRA and sunsetting the LPO, the central policy driver is also being gutted; the vision is being erased.

PUCs have been hesitant to approve new nuclear in regulated markets, and utilities have been leery of potential impacts to credit ratings when announcing new projects, in part because of overruns experienced at Vogtle 3 & 4. Without a government program aimed at addressing cost overruns, it is unlikely that projects can move forward in regulated markets.

In some States, energy policy provides opportunities for nuclear investment in the absence of federal support. Many states have deviated from Renewable Energy Portfolios and switched to Clean Energy Standards, which include nuclear. In some cases, like Colorado, acknowledging nuclear as clean energy makes it eligible for low-interest financing programs and counts toward requirements for utilities.

There is a wide range of additional state-level policies that impact new nuclear construction. Some states have policies that support coal for jobs, which compete with new nuclear for capacity. Other states have moratoriums on building new nuclear plants or arbitrary limits on the size or location of new plants. Some have conflicting rules, such as supporting new nuclear power but banning the inevitable spent fuel from any facilities that don’t currently exist. States can support nuclear power through feasibility studies, site characterization, and direct grants, but to a lesser extent than what the federal government could provide.

Without significant amendments, the “One, Big, Beautiful Bill” will be ceding the federal government’s role in innovation and industrial policy to States and private firms. States with regulated markets will be in a better place to direct and provide incentives for nuclear deployment. States with deregulated markets will face other constraints.

Market Realities

The issue is not whether nuclear can compete in a completely free market. The majority of nuclear plants in the U.S. were built without the advantage of tax credits after all. Only, there is no such thing as a free market for electricity. Electricity markets began deregulating in the 1990s, and the process continued through the 2000s. The regional transmission operators CAISO, ISO New England, MISO, NYISO, and PJM are all outcomes of the deregulation movement, but none of them is a free market. The deregulated markets are considered competitive, but that competition is constrained by the semi-unique rules of each system operator. Because of these constraints, nuclear and other generation sources are not compensated for all of their attributes. Nuclear’s contributions to grid resilience, fuel security, and land-use efficiency, alongside its zero-emission profile, are often undervalued or entirely unmonetized in standard market designs. This means the markets are not dynamic in competition—the product is commoditized, while production is not. Competition exists at the level of the larger market, but the topology of the grid plays a larger role than the market as a whole. There is no market for decarbonization. “Cap and trade” and other tax schemes set on accounting for the social cost of carbon have failed in the past.

The topology of the grid defines the ability of any generator to compete. The location of a generating resource relative to transmission infrastructure and other generating resources impacts its ability to sell its power on the marketplace. Areas having more generation than demand and not enough transmission infrastructure to send power to load centers result in congestion. Prices to send electricity over transmission lines increase as congestion increases; this is called locational marginal pricing (LMP) or nodal-based pricing. The grid operator is constantly trying to commit the cheapest energy sources to match demand. However, if too many very cheap energy generators are located in the same place, getting that power out of the region becomes difficult. Transmission lines can only transport a limited amount of electricity flow. The closer the electricity flow gets to the transmission line’s limit, the more expensive it is to send an additional unit of electricity across the line. Think of it as highway congestion pricing, except electrons are moving at the speed of light. If a line reaches its carrying capacity and gets too congested, it could trip a breaker, and the line will stop transporting electricity. This will cause a flurry of activity and emergency actions to reroute power around the inoperable line. To avoid this, grid operators monitor congestion at nodes across their entire region, committing resources and shutting down others to maintain electricity production while including both the costs of generation and transmission in mind.

Investment decisions for new generation in deregulated markets are influenced by expected prices of generation and other non-energy products. Subsidies and tax credits can artificially lower the price of energy generation for new and existing projects. The phase-out of tax credits and the sunsetting of the Loan Program Office will increase the expected costs that new nuclear projects will incur. This new set of expectations will affect the makeup of the next cohort of generation being added. As data centers, cryptomining operations, and electrification increase demand for electricity, nuclear will be less desirable from a cost perspective than natural gas.

Strategic grid planning, or lack thereof, can mean that previously competitive plants, including nuclear facilities, can be undercut on a single grid node by new, often subsidized, entrants or transmission congestion that disadvantages them. Even existing, fully amortized nuclear plants don't always compete effectively on price alone in wholesale markets, particularly in regions with low natural gas prices or high renewable penetration that suppresses market-clearing prices. The Quad Cities nuclear power plant houses two reactors that were planned to be shut down due to the economics of their grid location. Sandwiched between wind turbines and an inadequate transmission system, the Quad Cities reactors often faced negative energy prices, meaning the plant would have to pay to send its energy to the grid. The reactors were scheduled to be decommissioned in 2018, but were saved by the Illinois legislature’s passage of the “Future Energy Jobs” bill in 2016. Other reactors were not as fortunate; twelve reactors shut down between 2012 and 2021, most of which were in competitive markets where renewables and cheap natural gas put downward pressure on generation prices. With the resurgence of electricity demand, Palisades, one of the previously shut-down reactors, is planning to be restarted and recently received funding from the LPO to help move the process forward.

Return of the Demand

The U.S. electricity market had flat demand for decades. Recent projections for soaring demand, driven in part by data centers and AI, have taken a lot of headlines. It is fair to ask if market pull, driven by growing demand, will be sufficient to support energy abundance and a buildout of new nuclear energy.

Figure 2: Historical and projected electricity use in TWh. Sources: EIA, NREL, and S&P

Some utilities, mostly in cost-recovery regulated markets, are considering new nuclear in integrated resource plans (IRPs). These typically 5-year plans are a necessary step in the public utility commission (PUC) approval process for regulated utilities. IRPs are often represented as multiple pathways and are not firm commitments. For example, Duke, Dominion, Southern, and Florida Power & Light all have experience operating nuclear plants, expect dramatic demand growth, and are in regulated cost-recovery markets. They have hinted at building new plants at existing sites, but have yet to fully commit. TVA, which has been working toward building a 300 MW SMR for years, previously stated that the goal would be to build 20 reactors, not one, but still hasn’t given final approval for the first reactor.

In response to expected demand growth and increasing prices caused by scarcity, industries are trying to solve their own supply problem. Many first-movers are tech companies like Google or Amazon that support new advanced reactor designs. These initial agreements are largely predicated upon the existence of the tax credits, and will evaporate if the credits disappear.

Even if these early projects are built without tax credits, their demand alone is insufficient to achieve scale. The industry will build a few one-off projects and fizzle out. There needs to be a pathway to get utilities that serve most of the load in the U.S. to commit to order books of multiples, very likely through a consortium approach, to ever get to scale and down the cost curve.

Utilities know that long-term operation of nuclear plants provides low-cost, firm, reliable, and abundant electricity. Due to a combination of timing and availability to start building new nuclear, licensing timelines, and first-of-a-kind price point and project risk, there is no guarantee that new demand will simply result in significantly more new nuclear. Most likely, fossil fuels, particularly gas, will scale up faster due to availability and price. Delivery of new gas turbines due to high demand from utilities is now pushed out to 2030.

Dramatic increases in projected electricity demand, and likely rising electricity prices, will result in some market pull for new nuclear deployment. The market will likely wait to see if the demand is durable before committing to a very long-lived nuclear power plant. The result of relying on demand growth alone will be, at the very least, a delay to large-scale deployment.

Resetting the Market, or Failure to Plan?

The last time we were on the threshold of a so-called nuclear renaissance, gas was super cheap and became the primary energy source being built, undercutting and killing nuclear projects. One goal of the current administration’s “energy emergency” is to increase production of fossil fuels and further reduce gas prices. The proposed phase-out of investment tax credits increases the cost for new nuclear builds, driving investment away from nuclear and towards fossil fuels. The IRA credits and the LPO’s loan authority were always going to sunset. This would have moved investments away from nuclear anyway, but the reconciliation bill has an effect far greater than just the money.

It is common to hear people hypothesize that Trump's disruption of markets with tariffs or other EOs will shake things out and settle to a new normal with better terms. This implies some strategy, or at least a fundamental reworking through cutting, slicing, and taping back together.

We actually have a good idea of how the story will end if we return to business as usual for electricity markets of a decade ago. The energy market before the credits and other policy drivers was not conducive to a nuclear build-out. The one project that was completed only did so with the benefit of the 45J credit and LPO. Removing the credits and threatening the capabilities of the LPO reset the market to one that is less amenable to a nuclear buildout. Utilities and RTOs, already slow to commit, will be less likely to assume the risks and costs associated with nuclear. States, and potentially hyperscalers, will assume the mantle of decarbonizing through the deployment of nuclear energy.

Executive orders and declarations of “energy dominance” are not enough to manifest a nuclear fleet. A goal of 400 GW of new nuclear power is unattainable without a strategy, and not just a willing but an eager market. Meanwhile, the U.S. is falling behind international competitors. Instead of plans for plans, nuclear power in the United States needs a dedicated set of policies and an environment that enables the growth of the industry and the deployment of new reactors.