Do Renewables Lower Electricity Prices?

Lessons for an Energy Affordability Agenda

By Lauren Teixeira

Now that climate politics are out and energy affordability is in, renewables advocates are eager to show that wind and solar make electricity cheaper, actually—especially as those energy sources face a full-frontal assault from the President, who has not only sought to tax renewables but tarred them as “too expensive” and “the scam of the century.”

The resulting flurry of refutations—characterized by simple correlations, anecdotal evidence and ideologically-driven narratives about electricity markets—has laid bare the muddled state of energy resource discourse, with partisans on either side of the aisle completely talking past one another.

Democrats are often too quick to claim that, because renewables produce energy at zero marginal cost (the sun and wind are free), they are universally cheap—even going so far as to rebrand them as “cheap energy” in a new bill, the Cheap Energy Act, which seeks to restore tax credits for wind and solar projects. Republicans, meanwhile, tend to call out how integrating renewables into the grid requires extra spending in the form of transmission, backup generators, batteries and other equipment to manage changing power flows. Energy Secretary Chris Wright has suggested that for this reason, adding more renewables to the grid is “guaranteed” to make electricity more expensive.

One of the most frustrating features of energy resource discourse is the tendency of technology tribalists to focus on only a selection of factors that affect retail energy prices. Renewables can indeed lower the costs of some retail electricity inputs, like wholesale energy, and raise the costs of others, like capacity and ancillary services. But true affordability hawks should care only about the net affordability benefit of renewables.

What we actually know about the impact of renewables on retail electricity prices

Isolating the affordability effect of putting more renewables on the grid is hard. Electricity is complicated and a huge variety of factors influence how it is priced. In deregulated markets, retail electricity prices reflect not only the cost of energy procured on the real time and day ahead markets, but energy procured via fixed contracts (including short term hedging contracts, power purchase agreements, etc.); capacity payments and ancillary services (which are needed to balance the grid and ensure reliable 24/7 service); taxes and surcharges; transmission and distribution (whose costs can be very significant due to the need to harden against wildfire and extreme weather events); and the nature of retail competition.

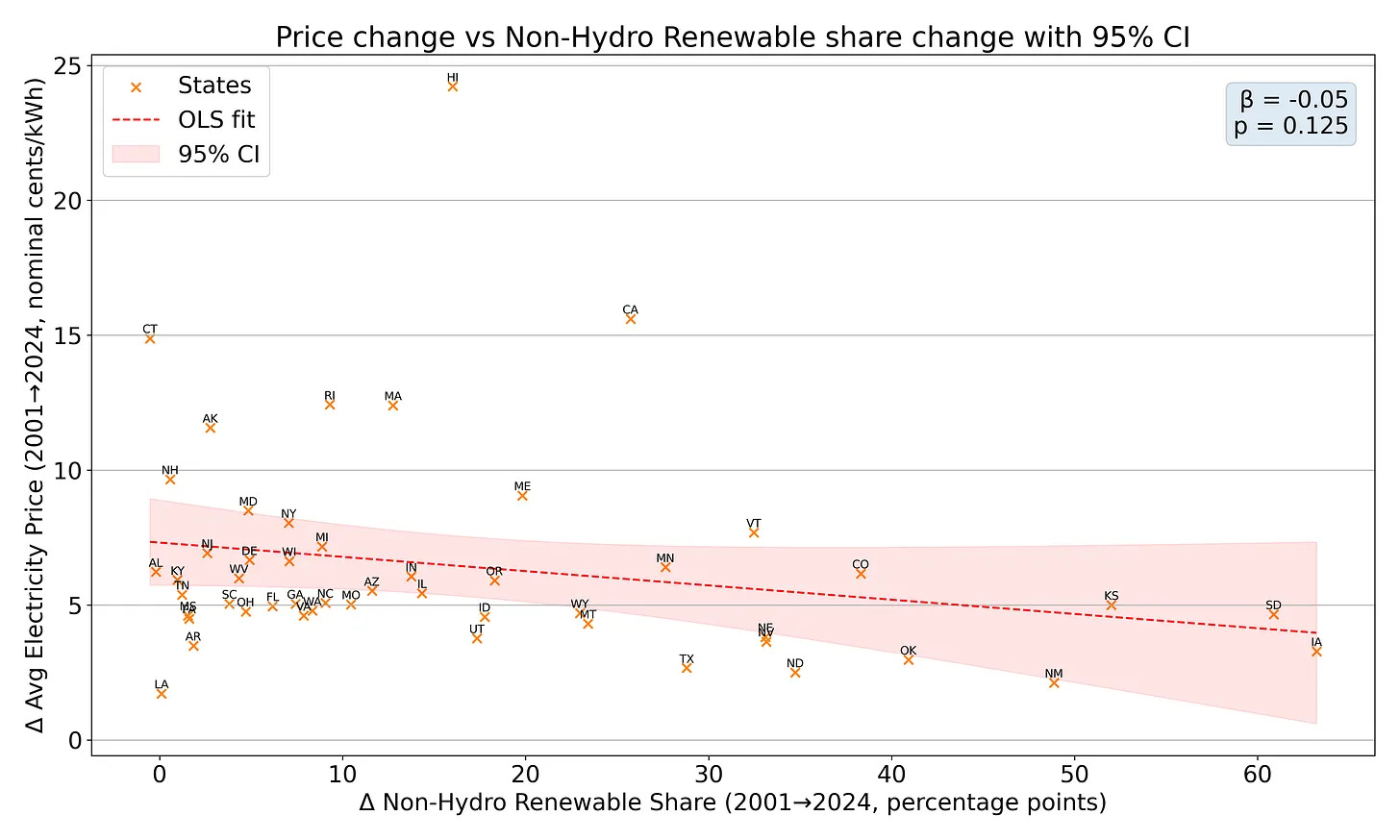

Because so many factors influence retail electricity prices, models that seek to explain price changes in terms of renewables share alone are not sufficient to establish any kind of causal connection between generation type and price. Yet this is exactly what renewables defenders have been offering. A couple of weeks ago, Politico published an analysis purporting to debunk President Trump’s claims about the effect of wind and solar on prices; what the analysis showed was that in June 2025, some states with a high renewables share had lower than average retail electricity rates—a classic example of refutation by anecdote. Earlier this summer, Breakthrough’s former Climate and Energy Director Zeke Hausfather also published an analysis showing a negative but not statistically significant correlation between change in renewables share vs. change in retail price. Despite not controlling for any other factors, the analysis was widely shared.

A new study from Lawrence Berkeley National Laboratory (LBNL) takes a much more robust approach by accounting for the dozens of factors that might plausibly influence state level retail electricity prices. Although their methodology and data are not faultless—a fact the authors, Wiser et al., freely admit—their work represents a major step forward in sophistication for our understanding of the effect of renewables on prices.

What they find is that renewables are maybe good for affordability but only if they’re put on the grid by market forces rather than by fiat. Wiser et al. find that, all else equal, over the 2019-2024 study period, an increase in penetration of wind and solar had a negative but not statistically significant effect on prices. A ratcheting up in Renewable Portfolio Standard (RPS) requirements, however, was associated with a small but significant increase in prices.

The intuition behind this finding is that states seeking to comply with their RPS requirements are procuring renewables that they would not have procured under a competitive market. These states may have poor wind and solar resources, which means that getting the required percentage of renewables on the grid requires excessive overbuilding and curtailment, importing out of state renewable energy credits at a premium, or even more balancing capacity in the form of expensive gas peakers. In such states, building renewables to match an RPS is simply not a good investment. As Hausfather documented for California several years ago, renewables can also exhibit striking value deflation effects: the value of an extra MW of wind or an extra MW of solar generation to the grid declines with each marginal megawatt installed.

But the fact that there are states that have continued to build wind and solar in the absence of active RPS’s demonstrates that there are places in which renewables are indeed a good investment. Texas, for example, satisfied its RPS in 2010 but has continued to build vast quantities of wind and solar in the years since. North and South Dakota have no RPS’s to speak of but have greatly increased their renewables share over the past five years. All of these states have experienced a decline in retail prices:

The key factor here—and one consistently lost amidst technology tribalism—is the extreme heterogeneity of renewable resources. Because wind and solar resources are better in some places than others, citing a particular successful instance of renewables deployment as evidence that renewables are “cheap” does not make much sense. The only thing that Texas’s success integrating renewables into the grid shows us is that renewables are a good option for Texas. But what is good for Texas is not necessarily good for New York.

One final thing to note about the Wiser et al. study is it does not take into account the effect of wind and solar subsidies. This is reasonable because the point of their study was not to determine if wind and solar are cheap but to simply parse out drivers of recent price trends. However, the study may overstate the (already weak) affordability effect of renewables, as some of the cost of producing renewable energy does not show up in electricity rates but on taxpayer bills; a full accounting would incorporate these costs.

Generation mix is only part of the picture

One problem with the incessant focus on particular generation sources is that it obscures the many, less sexy contributors toward rising electricity prices that do not have much to do with generation mix at all. Indeed, in most localities, energy costs account for less than half of one’s bill, the rest going to transmission and distribution as well as other surcharges.

Renewables did not place first, second or even third among the most explanatory variables in the Wiser et al. study. The single most important contributor, the authors found, was simply the influence of California—utility spending on considerations unique to the state like wildfire mitigation and liability insurance, which has ballooned as catastrophic wildfires have become more common.

The second and third most explanatory variables had to do with load. Because utilities recover their fixed costs (transmission, distribution etc) by spreading them over many customers and kilowatts, a sharp decrease in customer consumption will generally raise prices, while a sharp increase will generally lower them. And this is exactly what Wiser et al. found: an increase in behind-the-meter solar and energy efficiency uptake—which decreases demand for grid electricity—was associated with a statistically significant increase in prices, while an increase in overall load was associated with the opposite.

The Wiser et al. study sought to explain variation in state-to-state price trends; but if you want to know what is driving rising electricity prices overall, you have to look at utility capital spending.

A report by Wiser’s team and consulting firm The Brattle Group that came out in October 2025 finds that, while spending on generation has fallen everywhere, and spending on transmission has varied across regions, utility capital spending on distribution—the poles and wires that bring electricity from substations to home and businesses—has risen across every region of the country, and sharply: up 35% from 2019 in real terms.

Increased spending on distribution, unlike increased spending on transmission, is not plausibly related to increases in utility-scale renewable share generation (although it can be related to an increase in rooftop solar penetration, because when households are injecting electrons back into the grid, utilities may need to upgrade transformers and reconfigure circuits to handle bidirectional flow). According to the report, most of the increase in distribution spending was related either to resilience investments—hardening the grid against storms, wildfires, etc—or simply replacing aging infrastructure, most of which was first constructed in the 1960s and 70s and now approaches the end of its lifecycle. And thanks to bottlenecks in post-pandemic supply chains, reconstructing and refurbishing all of this infrastructure is a lot more expensive than it would have been even ten years ago.

What is the affordability hawk to do?

None of the above will be very satisfying for those who are interested in blaming rising electricity prices on a particular generation technology. The drivers behind the recent increase in prices are multi-factorial and geographically heterogeneous. Any serious affordability agenda will have to reckon with this complexity.

On the generation side, such an agenda would remove policies that stack the deck in favor of particular energy sources. Such policies distort markets and burden consumers. State renewable portfolio standards may have once served an important function by bringing renewable technologies down the learning curve; but those technologies are now mature, and RPSs, insofar as they remain, seem to be inflicting inefficient quantities of renewables on the grid, burdening consumers. For the same reason, federal tax credits for wind and solar should not be restored; they muffle price signals and inevitably result in a sub-optimal generation mix. The Trump administration’s attempts to kneecap renewables and bring back coal, which has long since been outcompeted by natural gas, are not any better.

Rooftop solar subsidies are similarly insidious. In California—which, to its credit, finally ended its lavish net metering 2.0 policy in 2023—rooftop solar subsidies have raised the state’s already already eye-watering electricity rates by an estimated 2.5 cents/kwH over the past five years. Policies that benefit a select group of adopters (mostly richer people) while raising prices for everyone else do not make for a durable energy affordability regime.

But generation is less than half of the picture. Bringing electricity rates down will require just as much, if not more, focus on the transmission and distribution piece of the puzzle. This may involve streamlining permitting for efficient long-distance transmission; performance-based ratemaking to rein in excessive utility capital spending perversely incentivized by cost-of-service regulation (“goldplating”); and more. In wildfire-prone states like California, it may involve shifting the costs of extreme weather preparedness off of utility bills and onto public balance sheets and the bond market.

Hopefully, affordability hawks on both sides of the aisle will be able to put aside their fixations on particular energy sources and embrace a more holistic understanding of electricity markets. That would be a boon for both consumers and the country.

The affordability debate needs less ideology and more math. Wind and solar can indeed lower wholesale costs in the right geographies, but without firm, clean power to back them up, consumers end up paying more for storage, gas peakers, and grid redundancy. Germany’s experience proves that sequencing matters: retiring nuclear before fossil fuels locked in higher prices and emissions, besides causing unnecessary deaths. The cheapest electricity systems over time will be those that pair renewables and nuclear to drive fossil fuels off the grid—reliably and permanently.

Also, we do need to start having more concrete conversations about electricty: How much electricity ? For what? The energy requirements for smelting aluminum are very different than those of street lights and for lamps for domestic users.

A thought provoking article, So here's a couple of thoughts.

If your high tech computerized solid state energy system, is Stupider than a Lump of Rotating Iron, you're doing it wrong. Solar, wind and grid support equipment are technically capable of turning on a dime, accessing information from far off realms, using all the calculus and math known to man and AI. Yet they are making the grid more fragile and expensive for rate payers. What's up?

Stop writing Paeans to the Altar of the Wise Spinning Generator! A ton of steel on bearings is not the smartest thing ever.

There are companies like Apparent.com in California, which have demonstrated the tech to make solar and battery systems, even houses and VTG, actively support grid stability. 10,000 solar panels can pretend to be a spinning generator, and allow a grid operator to control them to protect the grid thru SCADA, just like grandpa's giant spinning generator. These solid state technologies are proven and installed spottily throughout California, Hawaii and Texas, and provide economic value to their owners. But they have been blocked from widespread adoption across the grid, because that would save billions per month to ratepayers, costing utilities some fraction of that. Moving money uphill to Wall Street is the system's default goal, absent leadership that could somehow overpower lobbying.

The utility industry says "We can't afford that-- it's Too Cheap!", and our captured regulatory system says "Yes Sir! Please keep that revolving door spinning, Sir.".

The fossil fuel cartel makes a couple of questionable claims. "We are the free market! Don't mess with the free market! We will optimize you!" Sounds nice but it's a bit naive. A cartel is the opposite of a free market. Wall Street's speculators optimize for their short term gain. Rent takers all over the system get govt protection as they divert activity to their properties. That's why a train that would cost $6 Billion in northern Europe, or $8 Billion in mountainous Taiwan, is slated to cost $125 Billion in California. Rent-takers and their Regulators Rejoice!

California has a casino called CAISO where speculators gather every afternoon to bet on when clouds will quench wind and solar farms. Frackers sell wee bits of gas at fabulous prices when Solar takes the day off around 4:20 pm, saving us from the manufactured emergency. You can watch the excitement on the App, "Iso Today", which shows spot prices at every big substation in California, real time. Unfortunately they omit Nuclear, the Party Pooper. Speculators can't bet against nuclear's 95% availability, downtime scheduled years in advance. Nuclear energy cuts down costs for consumers but is bad for fossil generators and utilities.

Never assume you can judge the value of a technology by what our Wall Street driven system decides to do with it. With leadership, advanced grid controls and nuclear would be widely implemented.

Don't assume the "Grid Modelers" hired by well-endowed institutions will ever like the look of something that would damage revenue for their employers. They are paid the big bucks to keep the profits stable, not the power grid. To actually fix our grid we should have more smart adaptive controls. Unfortunately no one can predict what happens in a complex system. If we insist on calculus models predicting what might happen, we will not advance beyond 1970's linear technology that could plausibly be modeled. We need less prophecy. More engineering! More adaptive system!