America’s Nuclear Order Book Is Large and Growing

Over 70 GW of new demand is in the pipeline, much of it for small and non-light water reactors from hyperscalers

Thanks to fast-growing electricity demand, especially from AI data centers, demand for new nuclear energy is rapidly growing. In this analysis, we identify 74GW of planned or new nuclear reactor capacity in the United States. While it is unlikely that all of that capacity will ultimately be built, if even a fraction of it is deployed it would mark a historic turnaround for the US nuclear industry.

Historically, a commercial nuclear project required a regulated utility to build the plant, own the asset, and recover approved costs through rates. That is no longer the main event when it comes to planned new nuclear development. Today, the profile of potential commercial nuclear buyers has diversified, thanks, in large part, to AI’s new energy demand. Companies building hyperscale data centers are responsible for 30 GW, or 41% of the 74 GW of announced or prospective new nuclear reactor capacity in the United States. That is more than double the 18% currently under order from utilities and public-power buyers. If utility-hyperscaler hybrid deals are included, the total share of the commercial pipeline drawn from hyperscaler demand is nearly half. Hyperscalers now dominate the firm middle of the pipeline and are the largest identified demand source among more tentative projects. That is a dramatic shift for an industry that, until recently, effectively only had one class of buyers.

Hyperscalers and data-center developers are looking for large amounts of reliable, clean electricity, and nuclear is one of the few technologies that can plausibly provide firm power at that scale. But the story is not simply that AI demand will rescue nuclear. Nor is it that hyperscalers will replace utilities as the primary driver of nuclear project development. The reality is more complicated: non-utility buyers are creating much of the visible demand pressure, while utilities and public institutions still provide much of the deployment interface. In short, commercial nuclear demand is shifting away from decades of exclusive dependence on utilities and public-power buyers.

The technology mix is diversified too. The emerging pipeline is not simply a repeat of the historical large-LWR buildout. Small reactors and non-light-water reactor designs represent the majority of new orders at most stages of the deployment pipeline, from firm orders to more tentative demand signals. Large LWRs remain important, especially by capacity, but a range of reactor designs are being matched to different buyers and use cases.

While the market for new commercial nuclear projects is no longer just a utility procurement pipeline, this transition is still in its early stages. Demand is real and more diversified than in the past. Much of it however, from both utility and non-utility buyers, and inclusive of both traditional large light water reactors and smaller non-traditional technologies, has not yet become firm deployment activity.

From Market Signals to Buildable Projects

To understand this market more clearly, we built a dataset of new U.S. commercial nuclear projects, programs, and demand signals, sorted by maturity. We separately track non-commercial projects such as research reactors, the DOE pilot program, and other demonstration projects–which generate operating data and reduce technical uncertainty but have a totally different deployment logic. Uprates to existing plants are also tracked separately.

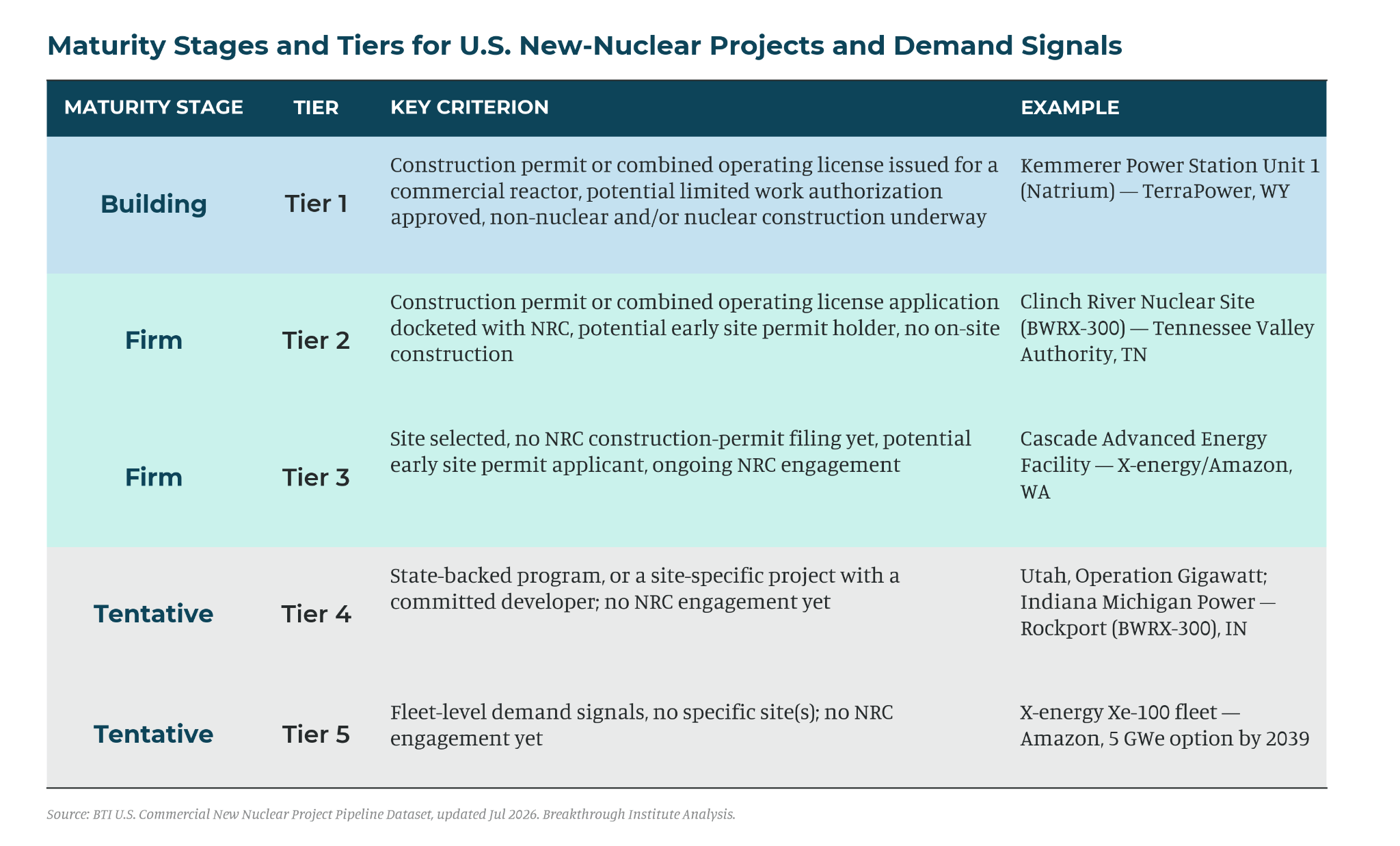

The dataset groups the commercial pipeline into three maturity stages: building, firm, and tentative, and five specific tiers. The building stage captures projects that have crossed a formal licensing threshold—with a site, a design, financing, and an issued license or permit—and may have construction underway. The firm stage covers projects with NRC-docketed applications or site-specific development with pre-application activities: not yet reactor orders, but the bridge between market signal and binding order. The tentative stage captures earlier activity—state-backed efforts, committed developers without NRC engagement, and broader demand signals like fleet-level agreements or non-binding capacity targets. Read from bottom to top, the tiers describe a conversion funnel: the stages a project must move through to get from demand signal (Tier 5) to actual build (Tier 1).

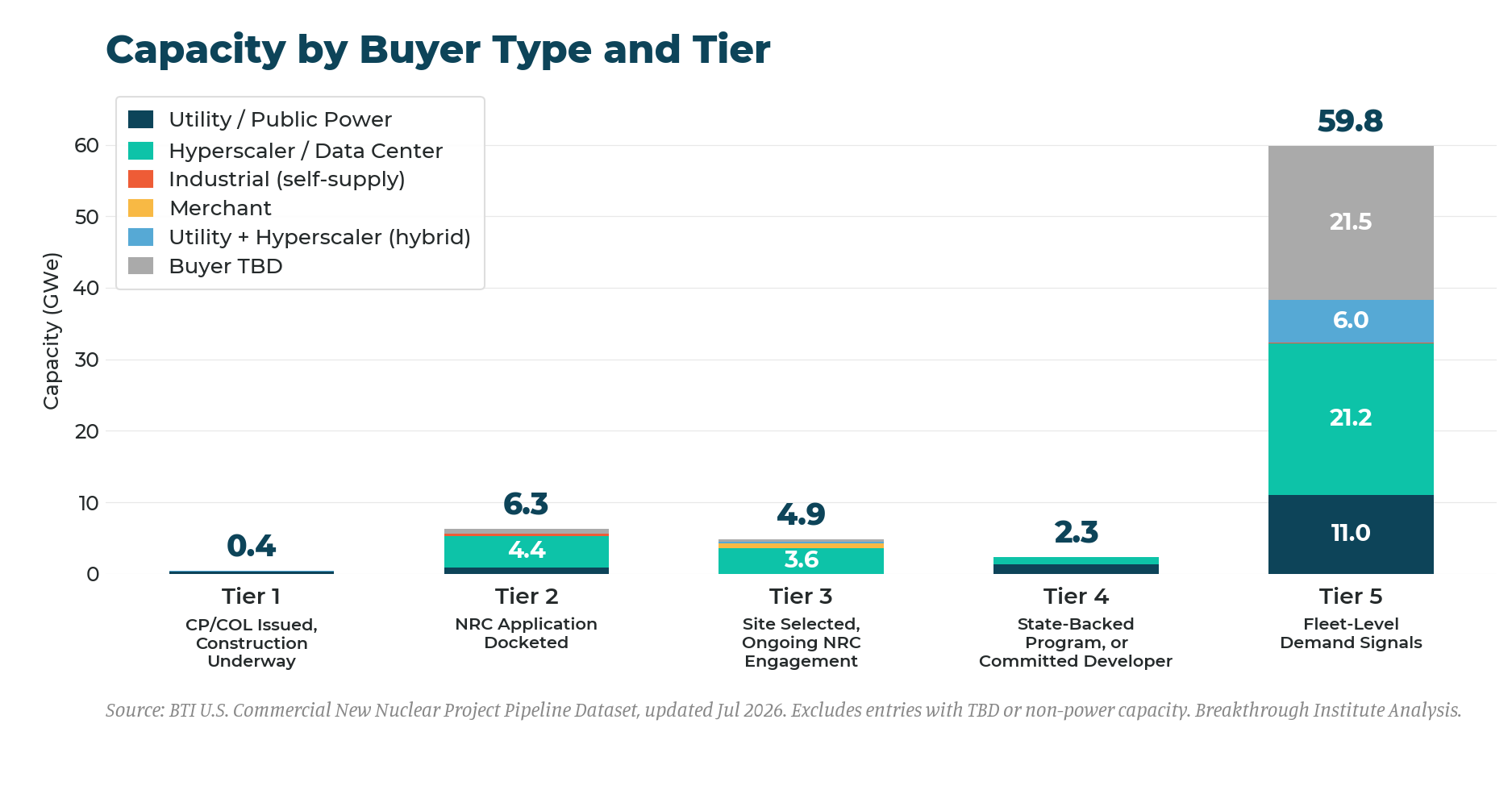

As shown in Figure 1, the United States has a broad commercial new-nuclear pipeline mainly because Tier 5 is so large. Nearly 60 GW of announced or prospective capacity sits in fleet-level demand signals, while the more mature tiers remain comparatively small.

The enormous amount of capacity in Tier 5 especially demonstrates the changes in the U.S. nuclear reactor customer base –hyperscaler-linked demand is now a major part of the commercial pipeline. Hyperscalers now have a direct stake in 45% of announced or prospective commercial capacity of the roughly 60 GW in Tier 5. Hyperscaler-only entries account for about 21 GW, or 35%, while utility-hyperscaler hybrid deals add another 6 GW, or 10%.

That demand from hyperscalers is not confined to one corner of the pipeline. Hyperscaler-linked entries appear prominently in Tier 2, Tier 3, and Tier 5. This tells the story of a market in transition: hyperscalers are now one of the most important sources of visible market pull for new nuclear, but much of that pull remains upstream of orders. They are reshaping the demand landscape faster than new reactor projects are moving toward construction.

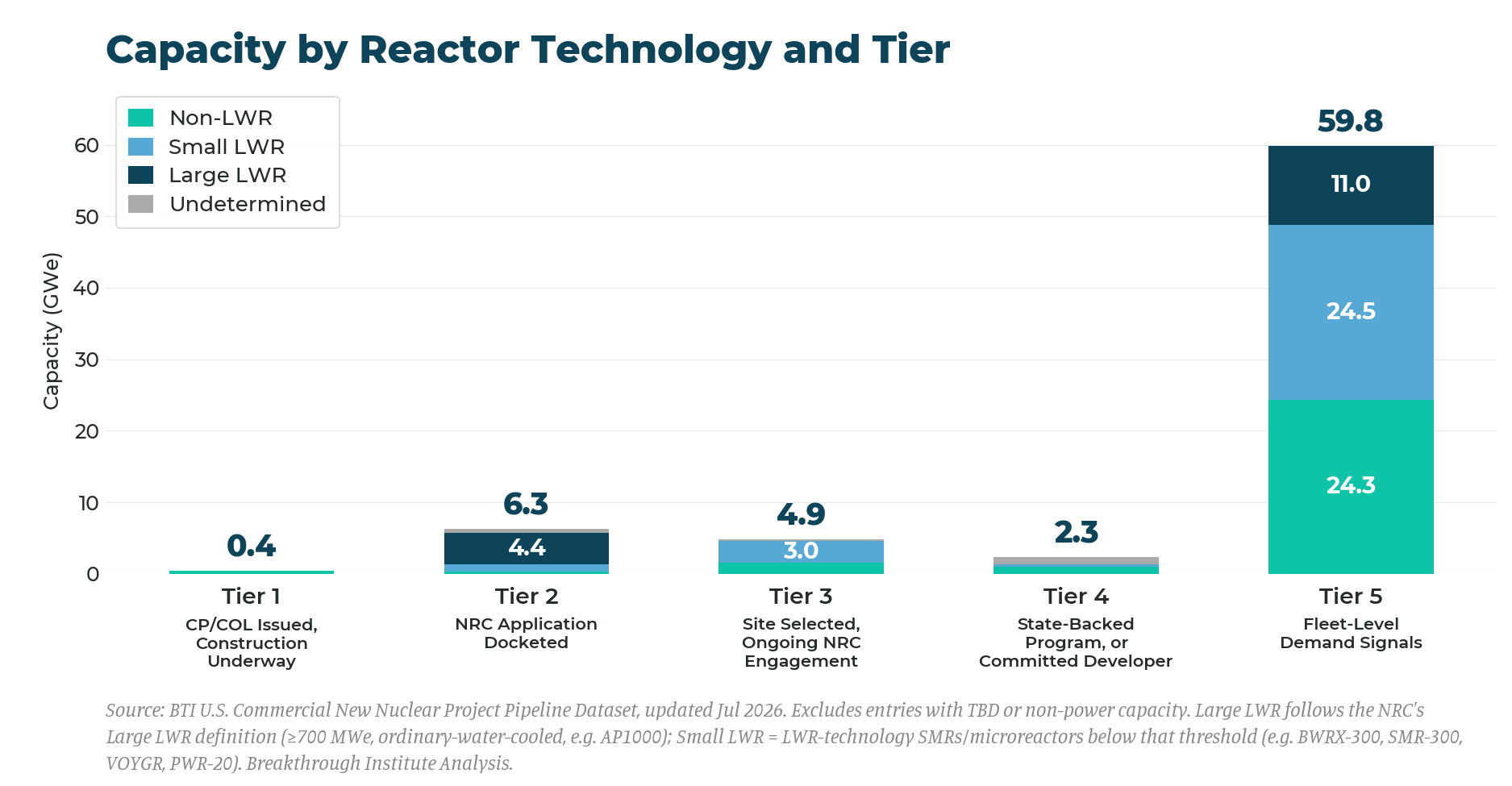

These new buyers are also influencing the technological mix of U.S. nuclear. Figure 2 shows that the demand pipeline is not simply a return to large LWR deployment. Across all stages and tiers except for Tier 2, small LWRs and non-LWRs account for most announced or prospective capacity, even though large LWR units are much bigger individually. This suggests that even where large LWRs remain significant, the pipeline is far more technologically diverse than the historical U.S. buildout. Also, buyers for non-LWR and small LWR are mainly hyperscalers. That suggests hyperscalers are not just adding demand to the traditional LWR market; they are disproportionately shaping the advanced-reactor demand to seek firm clean power.

To some, the hyperscaler demand pull is nothing more than a mirage. But rather, these early shifts in reactor demand should be understood as evidence that the U.S. is in a market formation process: the demand has arrived well ahead of the technological products, regulatory certainty, supply chain maturity, and financing support. Importantly, the demand for nuclear from hyperscalers is not only showing up in speculative new-build announcements. It is already showing up in the existing fleet, where capacity can be delivered faster. Hyperscalers are the clear catalyst behind the latest restart, uprate, and existing-capacity deals with a total of 8.3 GW of existing-fleet nuclear capacity: roughly 6.3 GW through existing-plant power purchase agreements, about 1.5 GW through restart-linked agreements, and about 0.5 GW through uprate-linked deals. In other words, that existing-fleet activity confirms the market pull is real, while the larger new-build opportunity remains earlier in the formation curve.

Still, this new demand is in an early stage. Fleet-level agreements, commercial frameworks, and high-case capacity targets are not yet build orders; they still have to become site-specific, financeable, and licenseable projects, and many early-tier entries even lack identified buyers.

A Matrix of Orderbooks

The next generation of U.S. nuclear projects will not be built only by vertically integrated utilities ordering large reactors one at a time. Utilities will remain central, especially for grid-scale deployment, but they will not be the only source of demand or project formation. Nor will the market be built by data centers alone. Hyperscalers may become major nuclear customers, investors, or partners, but they still need utilities, developers, regulators, suppliers, and operators to turn demand into electricity.

The more likely future is a matrix of orderbooks: repeatable project structures matched to different use cases. Large reactors may be best suited to bulk power, regional load growth, and large industrial or data-center corridors. SMRs may fit public power systems, coal-site replacement, utility-mediated data-center demand, and certain industrial applications. Microreactors may scale first through defense, remote, and critical-infrastructure markets.

The point is not to pick a single winner. It is to create repeatable combinations of reactor designs, customers, sites, financing structures, and licensing pathways. Nuclear gets cheaper and easier to deploy when projects are not reinvented one at a time. DOE’s new American Nuclear Supply Chain Loans point in this direction. The program is not a final build order, but it is designed to support long-lead equipment for eligible projects and accelerate deployment of a standardized reactor design.

The data-center surge has changed the nuclear market in a way that is still difficult to measure but hard to dismiss. For the first time in decades, new nuclear is being ordered by large, fast-growing customers that need firm, clean, around-the-clock power at scale. Some announcements may become projects, others may not, but the sector is no longer waiting only on traditional utility procurement. In any case, nuclear deployment will only scale through a matrix of orderbooks across customers, developers, and utilities.

| A guest post by

|